Special March 2026 Edition: Q4 2025 Spend

This edition of Inside the Traveler Wallet explores Datafy’s Q4 2025 National Traveler Spend insights, with takeaways for how destinations can respond & the analytics trends to watch. Happy reading!

Written By - Anna Blount

March 2026

We spend a lot of time discussing the back-and-forth of travel demand being up or down. But is that really the question anymore? I think each destination already has a pretty good sense of that. What feels more important right now is what travelers are actually doing once they arrive.

People are still taking trips. They are still spending. What is changing is how they are spending once they get there.

And that shift is starting to show up in very real ways across destinations. Here is what our team is seeing in the latest data.

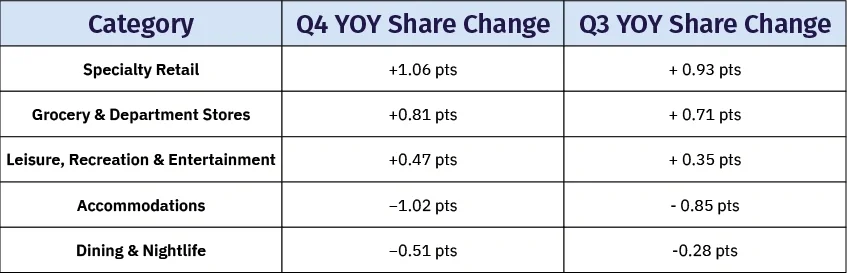

Q4 2025 Traveler Spending Insights

Traveler spending patterns in Q4 2025 reveal a clear dynamic across the travel economy. Travel demand remains strong, but spending decisions within the trip are becoming more selective. Travelers are still taking trips and spending more overall, yet they are increasingly managing everyday costs while protecting the experiences that make travel meaningful.

Overall traveler spend grew 6.74 percent year over year, well above overall inflation of roughly 2.7 percent. Because travel prices themselves increased by less than 1 percent year over year, much of that growth reflects real increases in travel activity rather than rising costs alone. In real terms, travelers are spending meaningfully more on travel, even as they make more deliberate decisions about how that money is spent during the trip.

Shifts in spending share across categories show how those decisions are playing out:

When the overall 6.74 percent growth in travel spending is applied to these shifts, most categories still show absolute growth in spending, even where share declined. The takeaway is not reduced travel activity, but evolving spending priorities within trips.

Source, Datafy Traveler Credit Card Analysis, Affinity

What this means for destinations

Travelers are managing everyday trip costs without giving up the trip itself. Dining and nightlife lost share while grocery and department store spending gained share, suggesting some travelers are substituting restaurant meals with convenience purchases or groceries during their stay. These adjustments appear to be cost management decisions, not signs of weaker travel demand.

At the same time, experiences remain protected. Leisure, recreation, and entertainment increased their share of traveler spending for the second consecutive quarter, reinforcing that activities and experiences within the destination remain central to why travelers take trips.

The data also points to diverging spending patterns across traveler segments. Specialty retail recorded the largest share gain for the second consecutive quarter, suggesting affluent travelers continue making discretionary purchases tied to the destination while more price sensitive travelers adjust everyday trip spending.

Taken together, these patterns reflect a K shaped spending dynamic, where higher income travelers continue discretionary destination spending while other travelers manage everyday costs within the trip.

How destinations should respond

Lead marketing with experiences, not logistics.Growth in Leisure, Recreation and Entertainment and Specialty Retail reinforces that in destination activities are driving travel spending growth. Destinations should emphasize experiences, events, and attractions in trip planning and marketing.

Emphasize value and flexibility for price-sensitive travelers.

With dining losing share and grocery purchases gaining share, many travelers appear to be managing everyday trip costs. Destinations should highlight casual dining, local markets, bundled attraction passes, and flexible itineraries that allow visitors to manage spending while still enjoying the destination.

Capture high-value travelers through premium experiences and retail.Continued growth in Specialty Retail suggests strong discretionary spending among affluent travelers. Promoting high-end shopping, curated experiences, and premium events can help destinations capture this higher value segment.

Analytics trends to watch in your Datafy dashboard

- Spending shifts across retail, dining, and experience categories

- Changes in destination spending tied to attractions and entertainment

- Differences in spending behavior across higher and lower value traveler segments

As we think about where things are heading, what stands out is not a change in whether people are traveling, it is how they are thinking about their trip.

People are still going. They are still spending. They are just making more deliberate choices about where that money goes. You can see it in the way experiences continue to matter, while everyday decisions become more flexible. You can also see it in how differently travelers are approaching the same trip.

To me, this is not about reacting to demand; it is about staying connected with the traveler and recognizing that not all travelers are experiencing this economy the same way. In a K-shaped environment, some travelers are doing more of the same while others are making more careful trade-offs, which makes thoughtful segmentation essential. The destinations that understand those differences and ensure the right travelers are receiving the right message, and prioritizing making the experiences offered feel worth it are going to be the ones that come out ahead.

The signals are already there. The people are there. Now it is about paying attention to them.

Interested in hearing more about our spending insights? Let's chat!

Methodology - This analysis draws on Affinity credit and debit card spending data from more than 90 million Mastercard, Visa, Discover, and American Express cards, filtered to include individuals traveling 50 plus miles from home. Spending reflects domestic purchases by American consumers. Margin of error, 0.02 percent to 0.04 percent.